ARTICLE

Market Recap – U.S. Leads Global Markets | 3rd Quarter 2018

by: Smith and Howard Wealth Management

Market Recap

Please note that this commentary was written prior to the recent market selloff and volatility. Please see our introductory statement for our thoughts on the recent market activity.

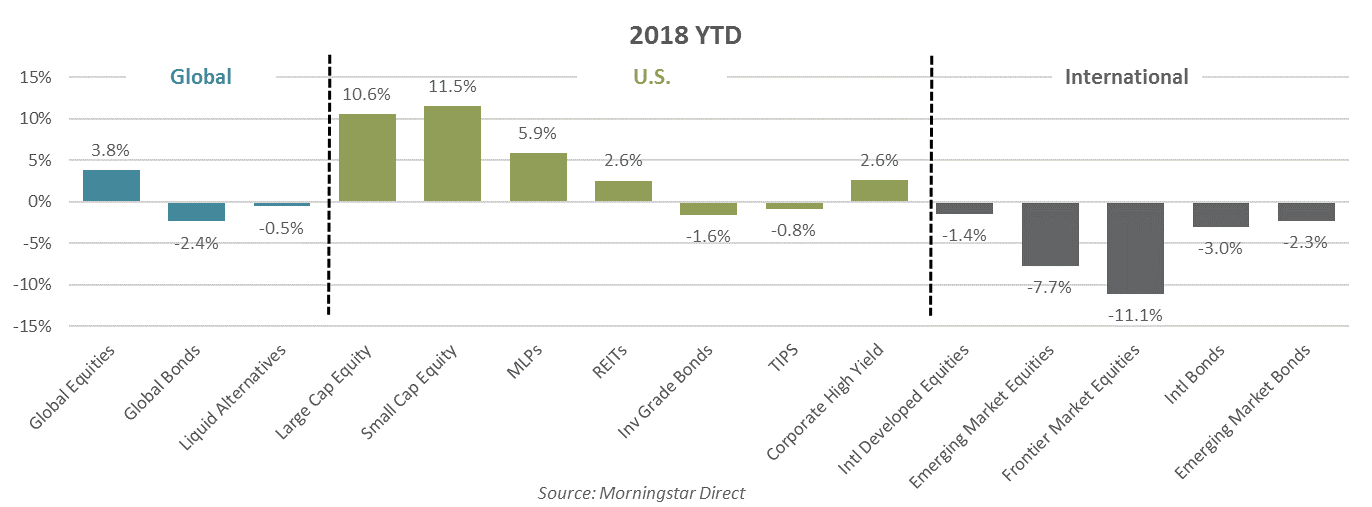

In a nutshell: Full year global market returns remained relatively modest, despite large gains in U.S. equities. U.S. investors understandably were focused on and encouraged by the strength in U.S. equities, but that strength unfortunately did not extend to bonds and alternatives, which remain flat to negative on the year. The strength also did not extend outside the U.S., as international equities were only modestly positive for the quarter.

For an in-depth look at the market for the quarter just ended, read below.

Gains in U.S. equities stole the spotlight during the 3rd quarter as they have on a year-to-date basis. U.S. investors understandably were focused on and encouraged by the strength in U.S. equities, but that strength unfortunately has not extended to other assets classes or market segments. The strength also did not extend outside the U.S. as international equities were only modestly positive for the quarter and remain negative for the year. As a result, global market returns remain muted despite the U.S. equity market representing a notable outlier.

Equities

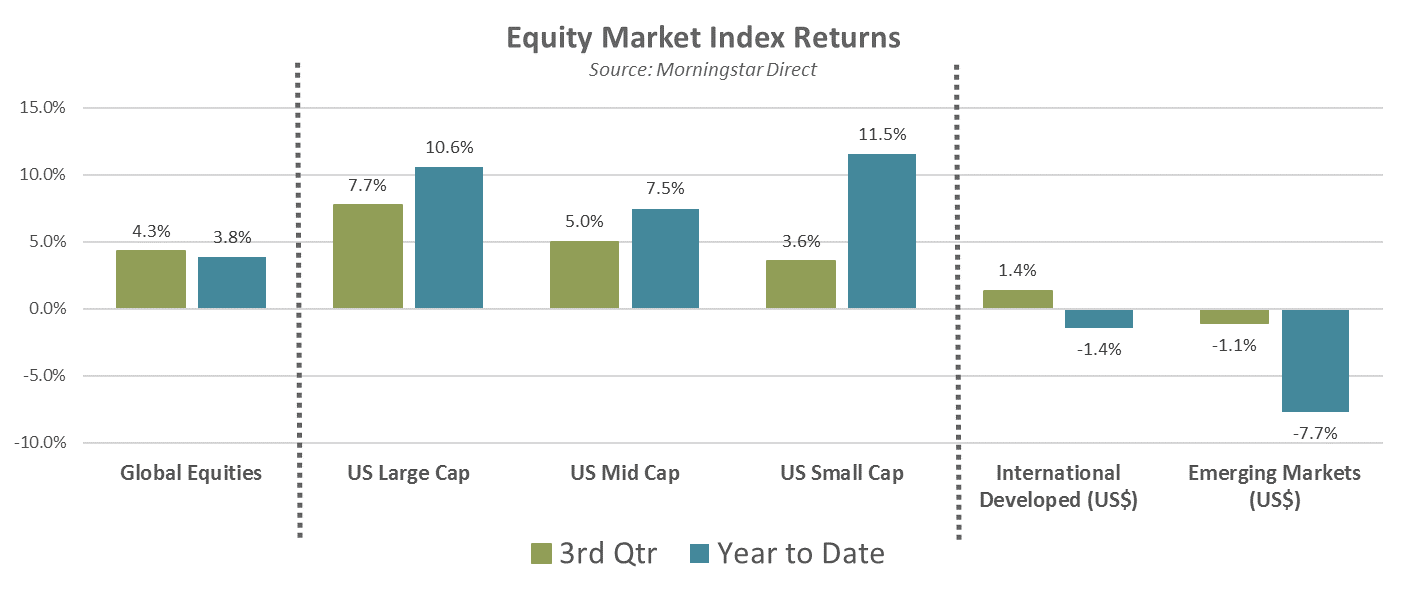

The global equity market advanced a healthy +4.3% during the quarter, which brought equity markets back into positive territory for the year (+3.8%). The strength during the quarter was concentrated in U.S. markets with returns strong across all market segments and styles. The most recognizable U.S. benchmark, the S&P 500, advanced an impressive +7.7% for the quarter. The strength unfortunately did not translate internationally, as developed (+1.4%) and emerging market stocks (-1.1%) were mixed.

Investors continue to try and decipher how those markets will be impacted by the threat of tariffs and higher U.S. interest rates.

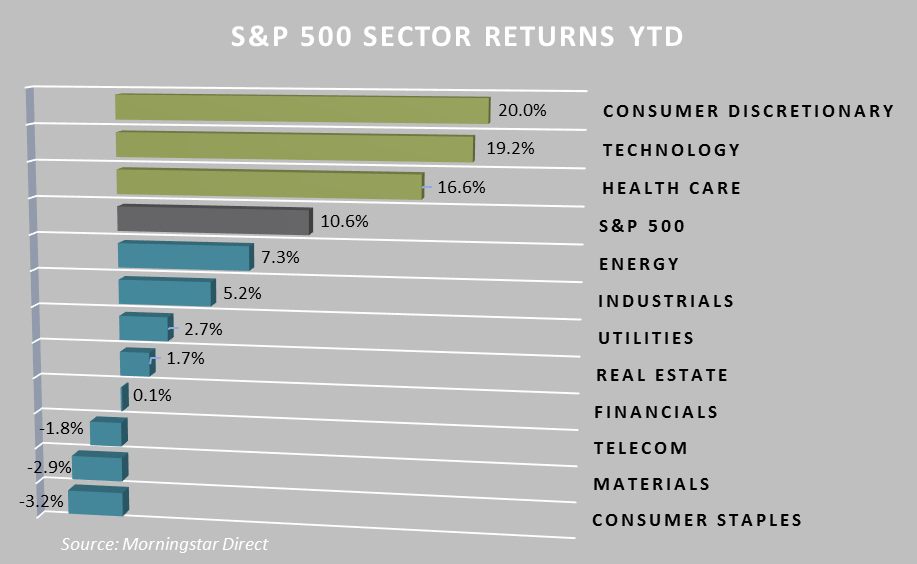

Perhaps hidden by the overall strength of the U.S. equity market is the increasingly narrow nature of the advance. As the accompanying graph illustrates, the strength is concentrated in just three sectors, with the other eight having an average return of only +1%. The same dynamic exists at the individual stock level, as well. The consumer discretionary and technology sectors are increasingly being driven by the performance of just a handful of stocks, notably Amazon, Microsoft, Google, Apple and Netflix. While every market cycle is different, professional investors do monitor “market breadth” and the adage is that narrowing “breadth” is a signal that a bull market may be losing steam.

Bonds

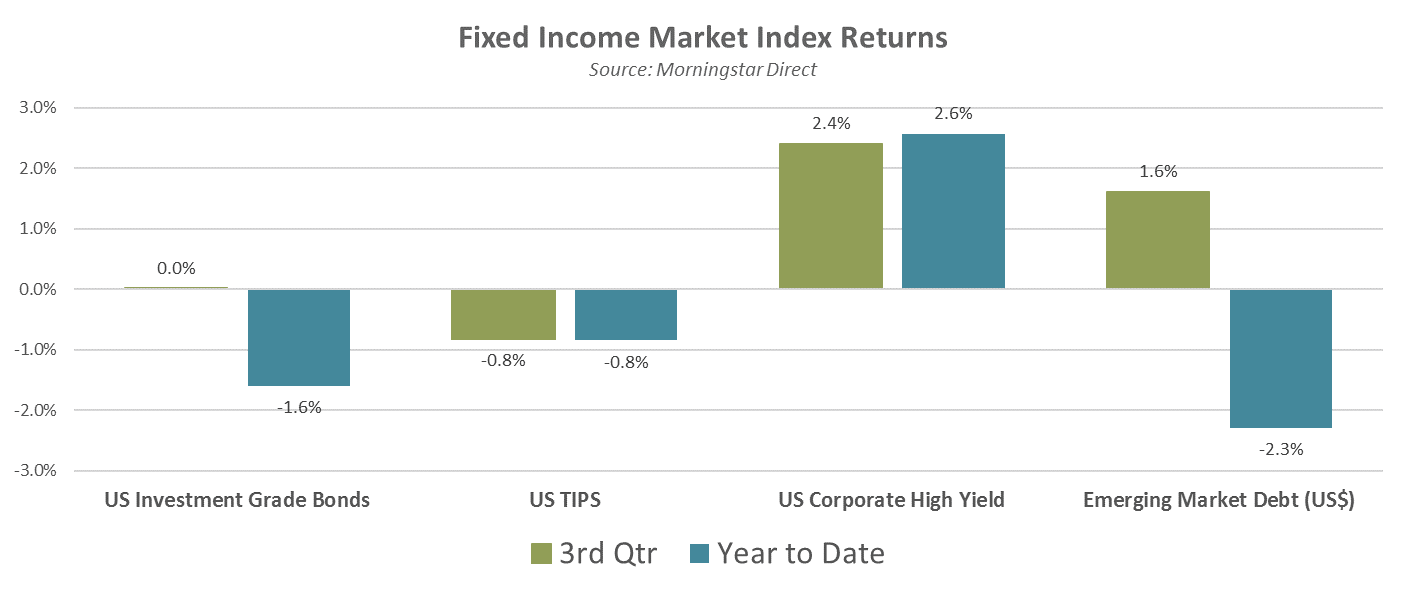

Yields across the maturity spectrum moved higher during the quarter as the period concluded with another interest rate hike by the Federal Reserve and inflation figures that continue to edge higher. The 10-Year U.S. Treasury yield climbed back above 3% in mid-September and has remained there after spending most of the quarter well below that level. Except for a very brief period in May of this year, the yield on the 10-Year is now at its highest point since 2011. Since higher rates have the effect of lowering bond prices and returns, the benchmark bond index (Barclays U.S. Aggregate) ended the quarter up just +0.02%.I

More opportunistic strategies, which often focus on lower rated corporate credit and non-traditional bond sectors, continued to fare well as credit spreads remained tight. With the exception of Emerging Market Debt, these strategies remain one of the few bright spots within fixed income.

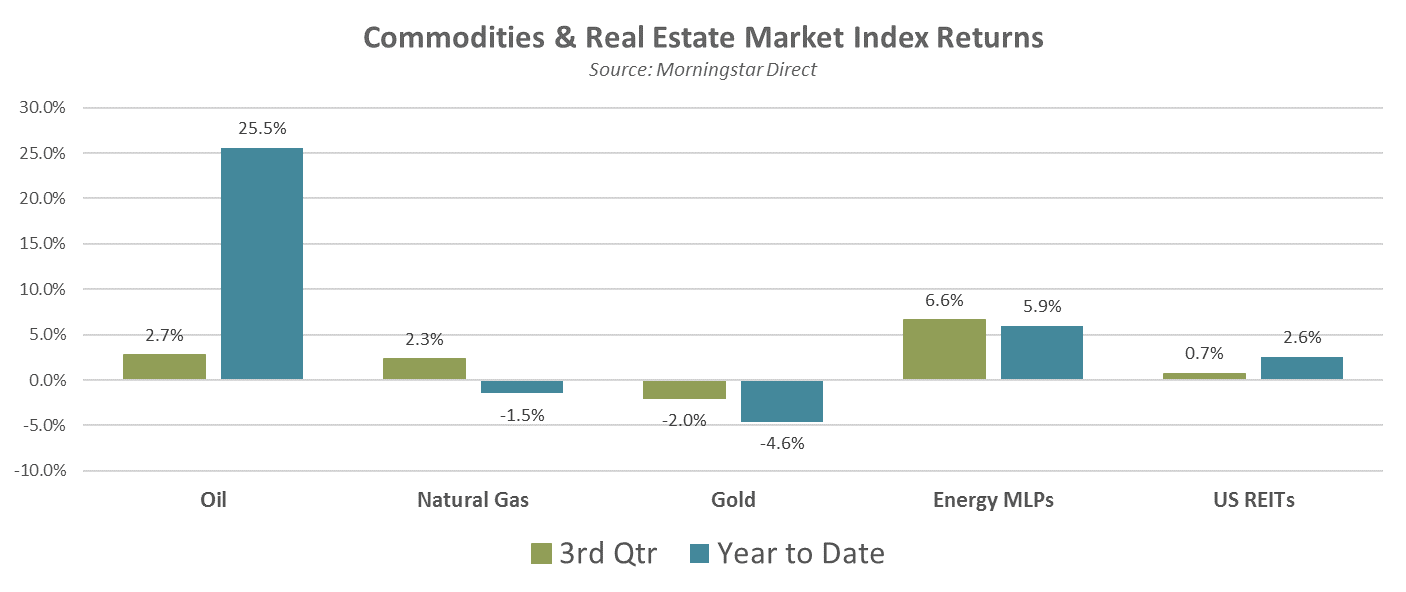

Real Assets – Commodities and REITs

While commodities and real estate related strategies have followed different paths than the fixed income and equity markets, the end results looking strikingly similar. Returns remain relatively low and unexciting with one outlier: oil. After reaching a low of around $26/barrel a few years ago, oil is back in the mid $70’s with some forecasters even pointing to the possibility of it reaching $100 again. Other commodities like natural gas and gold, however, remain range-bound and negative. Energy pipelines and REITs have fared better, generating modestly positive returns.

To learn more about how the markets may be impacted by the threat of tariffs and higher interest rates, contact Brad Swinsburg at 404-874-6244.

Explore more information on the third quarter of 2018 by visiting these links:

Market Outlook: Third Quarter 2018

On the Horizon: Third Quarter 2018

Deeper Dive: Third Quarter 2018

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

Back to Insights

Back to Insights