ARTICLE

Market Outlook – Stock and Bond Markets Got Cheaper During the Quarter | First Quarter 2018

by: Smith and Howard Wealth Management

Market Outlook

In a Nut Shell: Stock and bond markets may still not be cheap, but they both got cheaper during the quarter. While bond yields are still low from a historical standpoint, they moved noticeably higher over the quarter making them relatively more attractive to investors. The same can be said for equities. Flat equity markets with higher earnings figures indicates that investors are paying less today for every dollar of earnings than they were at the end of December. Both stocks and bonds may have entered the year with elevated valuations, but both ended the quarter at levels that are relatively more attractive.

For an in-depth look at the big picture, read below.

The Big Picture

The big picture for Smith and Howard Wealth Management is always going to be framed by valuations (see our previous article “Why Valuation Matters”). As long-term investors, we recognize that while it is interesting to speculate and debate about near-term events and breaking news, ultimately, investment returns are driven by valuations. Shifting portfolios towards cheap assets and away from expensive ones “wins” over time. It not only generates a higher long-term return, but typically results in smaller drawdowns or losses along the way. Put more simply, it’s the amazingly simple, but difficult to execute philosophy of “buy low, sell high.”

The Market May Not Be Cheap, But It Is Cheaper

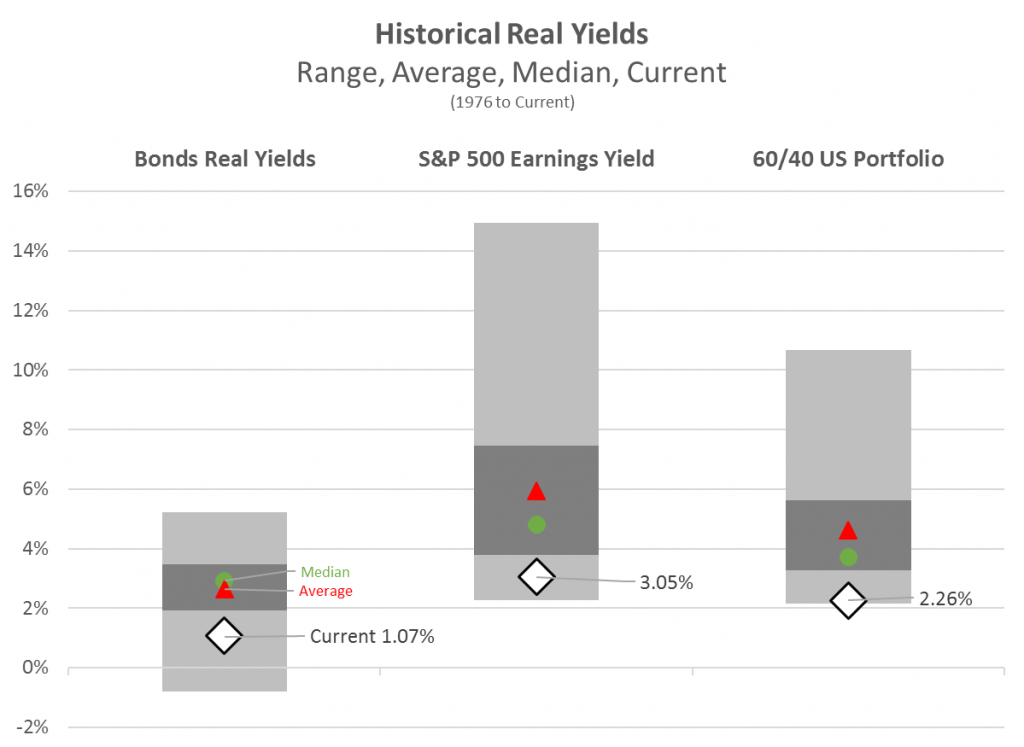

U.S. stocks and bonds are the centerpoint of client portfolios, as well as a critically important piece of the global economy. In the following chart we illustrate where current U.S. stock and bond markets are situated from a valuation standpoint relative to history.

Bonds Real Yields

The bar on the left related to the benchmark bond index shows that the current real yield (which is the quoted bond yield minus current inflation expectations) is roughly 1.07% (the white diamond in the lower portion of the bar). The height of the bar reflects the range of observations of this real yield over time going back quarterly to 1976. The “real yield” has been as low as –0.8% and as high as 5.2%. As one can see we are on the lower (more expensive) end of that bar. The same can be said for U.S. equities (S&P 500) in the middle bar.

S&P 500 Earnings Yield

Equity valuations also improved during the quarter, although depending on the metric one uses the degree is debatable. Without getting into the nuances of various earnings multiple calculations the big picture was that equity prices were down slightly during the quarter while earnings continued to grow and future estimates were revised higher. In the 4th quarter of 2017 (that was reported during this past quarter) 75% of S&P 500 companies beat earnings estimates and the aggregate earnings level rose an impressive 16%. This higher E (earnings) and lower P (price) means the price investors are paying for every dollar of earnings just got cheaper. As with bonds that doesn’t necessarily indicate the market is cheap, but for an investors outlook it should increase future return expectations.

60/40 US Portfolio

In this chart, we are also showing what the “Yield” is of a portfolio of the two assets combined into a blended portfolio (40% bonds, 60% equities). While both bonds and stocks on their own are expensive, they are also not at their most extreme levels (i.e. the diamond point for each is not at the lowest part of the bar). Interestingly though the portfolio combining both is close to its lowest point which means a blended portfolio of US stocks and bonds has rarely ever been more expensive. The reason for that is that through history when stocks were cheap, bonds were expensive. Conversely, when stocks were expensive, bonds were cheap. That is unfortunately not the case today.

A Silver Lining?

On a more positive note the bond and overall portfolio yields did improve over the course of the first quarter. The real yield on bonds increased from 0.75% at the end of December to 1.07% at the end of March. While this may not seem like an exciting number it is the first time it’s been over 1% in a number of years and is at least a premium over inflation for bond investors who have at times in the past been forced to settle for negative real yields.

As stated at the outset of this article, we are looking first at the U.S. markets and at a very high level. Given that high level valuations are still stretched, looking for less expensive “pockets” of opportunity within the U.S. and around the globe takes on greater importance. International equities, both developed and emerging markets, as well as various alternative strategies continue to present good relative value opportunities and/or returns less dependent upon markets continuing to simply go up. That has been and remains core to our strategy. While it is always more comfortable to invest closer to home, we must be willing and able to go where the returns are.

To learn more about the recent bond and equity yields, contact please contact Brad Swinsburg 404-874-6244

Explore more information on the third quarter of 2017 by visiting these links:

Market Recap: First Quarter 2018

On the Horizon: Seven Focus Areas

A Deeper Dive: The Impact of Rising Interest Rates

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

Back to Insights

Back to Insights